Keeping up with the Joneses

I'm not sure why this article focused on Utah; debt is not a problem unique to that state.

Also, I'm bothered that it failed to reflect the reason many people max out their credit cards: healthcare disasters.

I am particularly frightened by statistics that more and more people are choosing to finance their new homes with "interest only" loans. That shows an awful lot of faith in the future, that "something" will come along ...

My dad raised me on the Franklin aphorism quoted here. Even if the article is perhaps obnoxiously holier-than-thou, I thought it worth posting.

(Maybe because I feel defensive about driving a beat-up 1994 van and buying my clothes at Goodwill.)

Lagging Behind the Wealthy, Many Use Debt to Catch Up

By Bob Davis, The Wall Street Journal, May 17, 2005

Better to go to bed supperless, than wake up in debt. |

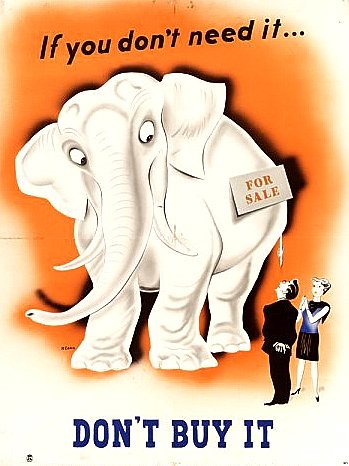

More and more Americans are turning to debt to pay for lifestyles their current incomes can't support. They are determined to live better than their parents, seduced by TV shows like "The O.C." and "Desperate Housewives," which take upper-class life for granted, and bombarded with advertisements for expensive automobiles and big-screen TVs.

Financial firms have turned credit for the masses into a huge business, aided by better technology for analyzing credit risks. For Americans who aren't getting a big boost from workplace raises, easy credit offers a way to get ahead, at least for the moment.

Since 1990, income for the median American household has risen only 11% after adjusting for inflation, while median household spending has jumped at 30%, according to an analysis by Economy.com. How could the typical family afford to spend so much? Median household debt outstanding leaped by 80%.

Last year, 28 of every 1,000 Utah households filed for bankruptcy, twice the national average and nearly triple Utah's rate a decade earlier.

Thomas Monson, the [Mormon] church's second-ranking leader, said he was "appalled" at advertising for home-equity loans that is "designed to tempt us to borrow more in order to have more." He repeated the words a Mormon elder spoke during the Depression:

Americans spent half the money from refinancing their homes in 2001 and early 2002 to pay for home improvements, cars, vacations and other consumer expenses, the Federal Reserve reports. Many other consumers relied on credit cards. U.S. households with at least one credit card owed $9,205 in 2003, a 23% increase from five years earlier after adjusting for inflation, says CardWeb.com Inc., which tracks the industry.

Cornell University economist Robert Frank sees house sizes, which have grown 30% since 1980, as an indication that middle-income Americans are battling to keep pace with the wealthy homeowners who build king-size McMansions.

In an earlier era, many people had no choice but to save first and spend later. Now, with credit, they can spend right away. For many young people, it's realistic to expect their earnings to rise.

Yet many fear credit has spread so widely that many Americans are overextending themselves, leaving a growing number anxiously in debt and, increasingly, bankrupt.

Concern about out-of-control credit is especially prevalent in Utah. Last month, Jay Evensen, the editor of the editorial page at Salt Lake City's Deseret Morning News, wrote a column blasting "people who wield their Visa cards like swords as they cut through the jungles of greed on a shopping crusade."

Robert Head, a Utah mortgage broker, reflects the state's ambivalence toward debt. He specializes in interest-only loans, which sometimes can leave people in over their heads. But at the same time he complains that too many Utahns suffer from what he calls "the Nephite syndrome," referring to a clan described in the Book of Mormon that was reduced to poverty through greed.

... using debt to try to move ahead has as many pitfalls as promise. Growing up in a small house crammed with as many as 11 kids, Winford Wayman, a 30-year-old construction worker, longed for privacy and open spaces. But he and his wife, Kristin, a 26-year-old bookkeeper, fell behind as they borrowed to buy pickup trucks. Mr. Wayman has purchased or leased four since 1999.

"I like trucks. They make them so damn good-looking. I see a good-looking truck and I have to have it," says the slender, goateed Mr. Wayman.

Technorati Tags: Greed, Credit, Debt, Folly

by melinama @ 5:40 AM

2 comments

![]()

![]()

A few of my daughter

Melina's great posts:

A few of my daughter

Melina's great posts:

2 Comments:

My husband and I worked very hard to get rid of our debt and work hard to save for our children's education and retirement. With our current income, we are considered "rich" so we pay alot of taxes. People who are living in big house, driving new trucks, taking extravagent vacations, etc, will they have enough for retirement or will my tax dollars go to help them? I don't mind helping people who need it, but you squandered your money when you were young, why should I have to pay for it? This may be an unreasonable fear, but only time will tell.

I agree so much money and energy is squandered because people try to live the life they think they are entitled to due to societal pressures and media exposure.

Also, I remember reading somewhere that over 50% of bankruptcy are filled by people due to medical expenses.

Post a Comment

<< Home